I am writing this in English and publishing it on Medium and LinkedIn because what is happening in Spain with housing should not stay a local, private frustration. It is a systemic problem in a European country that likes to present itself as modern, attractive and “open to talent”, while quietly making decent housing almost unreachable for its own working population.

I am almost 30. I have a degree, two master’s degrees, and I work in one of the most in-demand areas of tech. And still, like many others in my office, buying a home in Madrid feels closer to fiction than to financial planning.

This article comes directly from that office conversation: highly qualified people in good jobs, realising that the “adult milestones” our parents reached in their 20s or early 30s are now almost out of reach for us. Not because we are irresponsible or lazy. But because the rules of the game have changed.

And we need to start naming who is actually writing those rules.

You will find all articles and documentation at the end of this article.

1. Spain’s quality of life is falling. And housing is at the centre

Let’s start from the big picture.

The Observatorio de Intangibles y Calidad de Vida (OICV) recently published its 2025 report on social happiness and quality of life in Spain. The index has fallen again to 7.17/10, down from 2024 and half a point below the maximum reached in 2020. The three main factors behind the decline are very clear:

- the price of housing,

- corruption, and

- social integration.

In the most “tensioned” areas, residents rate the relationship between price, location and quality of housing at around 1 out of 10. The only regions that “pass” are low-pressure ones like Extremadura or La Rioja. Baleares, Madrid and Catalonia already have housing prices above the 2008 bubble peak.

At the same time, 40% of young adults under 30 report unwanted loneliness, and digital ageism hits three out of four older people. Housing is not just a financial problem; it is eating into social cohesion and mental health.

2. Prices vs salaries: when a basic need is priced like a financial asset

Data from the BIS (Bank for International Settlements) and the ECB show the scale of the distortion:

- Between late 2013 and Q1 2025, real housing prices in Spain have risen about 45%, while real wages have essentially stagnated.

- The ECB’s overvaluation index estimates that Spanish housing is now about 14.3% above its “fundamentals”, compared to around 10% in the Euro area as a whole. The jump of three percentage points between late 2024 and early 2025 is the fastest in the entire series outside the Covid anomaly.

- To buy a home, a Spanish household now needs around 7.8 years of gross income, according to the Banco de España.

Madrid and Baleares are at the top of the overvaluation rankings. CaixaBank Research, using the Bank of Spain’s accessibility ratios, confirms that in both regions the price of housing has clearly decoupled from household income.

On the ground, this translates into something very simple: in Madrid, a normal salary and a good CV are no longer enough. People with stable jobs are pushed to spend more than 40–50% of their income on rent, or to postpone buying indefinitely, while prices continue to run ahead of them.

3. The tax elephant in the room: when up to a quarter of the price is the State

One of the most uncomfortable parts of this debate is fiscal.

According to the Instituto de Estudios Económicos (IEE):

- Taxation on housing in Spain collects about 52 billion euros per year, roughly 3.5% of GDP.

- Around 20–25% of the final price of a home is taxes and quasi-fiscal costs.

A recent breakdown shows:

- A new home has 10% VAT on top of the price.

- A second-hand home pays ITP (Impuesto de Transmisiones Patrimoniales), typically between 6% and 10%, depending on the region.

- To that you add AJD (Actos Jurídicos Documentados), plusvalía municipal, IBI, ICIO, licensing fees, etc.

In practical terms, for a 300,000 € new home, if roughly 20% of the final price are taxes, that means the same home could cost around 240,000 € without them. The difference is practically the whole “entry ticket” that banks ask buyers to have saved.

And while housing is treated as a basic right in public discourse, Spain is:

- The second-highest country in the OECD in effective taxation on owner-occupied housing (around 30.3% effective rate vs 6.5% EU average).

- Collecting 3.5% of GDP via housing-related taxes while investing only around 0.5% of GDP in public housing and related programmes.

Regional data show the incentive very clearly: in 2024, communities raised a record 12.36 billion euros via ITP and AJD alone, and expect to go even higher in 2025 — not because they built more homes, but because prices went up.

If you design a system in which:

- every extra euro in the sale price means extra tax revenue, and

- you keep a scarce supply of land and housing,

then you create a hidden, but very real, incentive for the State to tolerate or even favour high prices.

4. Land, planning and the artificial scarcity of buildable space

Another part of the story is how much land can actually be built on, and who decides that.

The CEU-CEFAS report on the housing problem in Spain is very blunt: the crisis is “generated fundamentally from the State” through laws and policies that reduce supply and push prices higher. They highlight:

- slow and complex planning procedures,

- delays and uncertainty around permits and zoning changes,

- and episodes of political-administrative corruption linked to land reclassification.

In Spain, urban planning is heavily controlled by local and regional authorities. Only about 15–20% of land is classified as urbanisable in many areas; the rest is non-buildable by political decision, regardless of its real ecological value. That limited, administratively created “scarcity” is capitalised into higher land values, which then pay higher IBI and generate more tax when traded.

This matches the logic described in a TikTok I saw recently (yes, sometimes TikTok teaches something): if you “remove hamburgers from McDonald’s so that your salad looks cheaper”, you are not making food more affordable, you are just manipulating comparison points.

In Madrid, where demand is intense and wages are above the national average, this artificial scarcity is amplified. When you limit land, delay planning and stack taxes on top, prices can only move in one direction.

5. Vacant homes: 3.8 million empty, but not where young people need them

The paradox often mentioned is: “How can there be an ‘emergency’ if Spain has millions of empty homes?”

According to the latest estimates based on INE data and the Fundación Foessa, Spain has about 3.8 million vacant homes, roughly 14.4% of the total stock.

The BBC summarizes the situation:

- These houses are not in the places where demand is highest. Many are in rural or depopulated areas (Galicia, Castilla y León, etc.), far from where jobs are.

- A large number of empty homes are not habitable without major renovation that owners cannot afford.

- Others are stuck in inheritance disputes among heirs.

From a young worker in Madrid’s perspective, those 3.8 million empty homes might as well be on another continent. The mismatch between where housing exists and where people actually work is brutal.

6. “Okupación” and legal insecurity: small numbers, big impact on behaviour

Another uniquely Spanish element in this story is the debate around “okupación”.

During the pandemic, the government introduced extra protections against evictions for tenants in vulnerable situations, extending them repeatedly in the name of social emergency. The objective was protecting families with no income. Is legitimate. But the side effect is also clear:

- Eviction processes for non-paying tenants can take years.

- Some owners see themselves paying mortgages, community fees, insurance and taxes for properties where they haven’t collected rent for a long time.

Associations of small landlords describe how the risk perception has changed: if you believe that once a non-paying tenant is inside you may not be able to recover your home quickly, the rational reaction is not to rent at all, or to rent only to profiles considered “ultra-safe”, excluding many young people with temporary contracts.

The BBC article reminds us that official complaints for illegal occupation (allanamiento/usurpación) are about 16,400 per year, which is around 0.06% of all dwellings — statistically small, but symbolically huge.

So even if “okupación” is not the macro driver of prices, it feeds a climate of legal insecurity that reduces rental supply, especially in cities like Madrid where every flat counts.

7. Are big landlords really the main problem? Data say: not alone, and not everywhere

There is a very popular narrative:

“Housing is expensive because of big landlords and foreign funds.

If we control them, we fix the problem.”

Reality is more nuanced.

7.1. Who actually owns the housing stock?

Several recent studies show:

- 82% of housing owners in Spain own a single dwelling, and 97% of them live in it.

- Only about 4% of owners have three or more homes.

At the national level, data on “grandes tenedores” (owners with more than 10 residential units) show:

- Around 27,000 big owners hold about 1.046 million dwellings, roughly 4.3% of the total housing stock (about 27 million dwellings) — https://www.spanishpropertyinsight.com/2025/06/25/spains-housing-stock-surpassed-27-million-dwellings-for-the-first-time-in-2024/

- If you exclude primary residences, their share goes up to 8.9% of the “investment” stock, but still far from the majority.

In some cities:

- Bilbao has identified 2,915 dwellings in the hands of big holders, about 2% of the total local stock.

So, yes, there are big players, and they matter. But most homes and most rental properties in Spain are still in the hands of small owners. Ordinary people, not funds.

Even in the rental sector, an analysis of who holds deposits in some regions shows that entities classified as “mega-landlords” manage around 15% of the registered rental dwellings, not all.

7.2. The development side: a fragmented supply industry

On the new-build side, the picture is similar:

- The 10 largest developers in Spain will account for only about 12.5% of all new homes delivered between 2024 and 2026.

- The top 50 will deliver roughly 23%. The rest is extremely fragmented among small and medium developers.

There is no oligopoly that “controls all the supply”. The problem is that the total volume built is too low, not that a few giants produce everything.

7.3. So what are big landlords doing?

Big institutional landlords certainly shape prices in some micro-markets (certain neighbourhoods of Madrid, Barcelona or coastal zones), and their strategies matter. But the aggregate data suggests:

- They amplify tensions in already scarce areas.

- They do not explain why there is a structural deficit of more than 2 million homes projected to 2040, according to IEE estimates.

Blaming only “funds and big landlords” is politically comfortable, but incomplete. It hides:

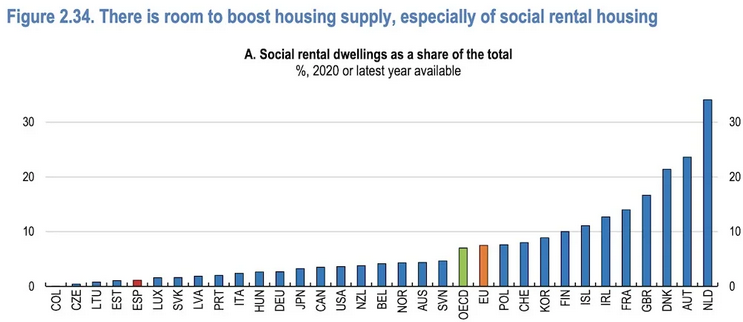

- decades of underinvestment in social housing (Spain has about 3.3% social housing vs 8% European average),

- very high taxation on housing compared to other OECD countries,

- and tight planning and land constraints that directly limit how much can be built.

Big landlords are part of the story, but not the whole story. And certainly not the only villains.

8. Madrid as an example of a broken equation

Let’s go back to Madrid, because this is where many of us feel the problem most intensely.

Putting together the data:

- Madrid is among the regions where prices have already exceeded the 2008 bubble peak.

- It is one of the communities with strongest indicators of overvaluation, alongside Baleares.

- It concentrates high wages, strong demographic pressure, tourism and a growing number of temporary residents (students, expats, digital nomads, etc.).

- The OICV survey shows residents in “tensioned” areas rating price–quality–location close to 1/10, reflecting an everyday sense of being squeezed.

On top of that:

- Spain has around 3.8 million empty homes, but very few of them in central Madrid where demand explodes.

- There are nearly 400,000 tourist apartments nationwide (~1.4% of housing stock), but in central districts of Madrid and other cities, their concentration can exceed 10% of all dwellings in some streets, clearly impacting local rents.

- Legal insecurity around eviction and “okupación” reduces willingness to rent long-term at affordable prices.

The result is an ecosystem where every structural element — prices, taxes, planning, tourism, legal uncertainty — pushes in the same direction: upwards on prices, downwards on affordability.

If you are a young professional in Madrid, you don’t need econometric models to understand this. You just need to open Idealista, look at your payslip, and do the maths.

9. We are not lazy. The game is rigged.

When people in their late 20s with degrees, master’s degrees and good jobs cannot realistically access a decent home without devoting most of their salary to rent or debt, it is not a “lifestyle choice”. It is a structural failure.

And yet, the public debate often tries to redirect the blame:

- To our parents’ generation for “speculating” with a flat and a small place at the beach.

- To any owner who dares to rent their property and asks for some guarantees.

- To “big landlords” as the only enemy.

Yes, there has been private speculation. Yes, abusive behaviour exists in parts of the market. Yes, some funds treat homes like chips in a casino.

But the data shows that:

- Most owners are small, and many of them are also squeezed by taxes, bureaucracy and legal insecurity.

- The State takes about 52 billion euros per year from housing while investing a fraction of that into truly affordable housing, and while keeping one of the highest housing tax burdens in the developed world.

- Planning decisions, land classification, eviction rules and tax structures are policy choices, not natural disasters.

In other words: the system is designed so that when your dream home becomes more expensive, someone in the public sector also earns more. That does not automatically mean “evil intention”, but it does mean misaligned incentives.

We work hard, we study, we upskill, we move to the cities where the jobs are, and still we find that the basic foundation of a stable life. Having a home keeps moving away from us.

At some point, this stops being an individual problem and becomes a political one in the deepest sense of the word.

10. Why I am writing this (and what I want you to do with it)

I decided to write this after another conversation in the office where we compared salaries, rents, mortgage simulations and… despair. Young people close to 30, with solid careers in one of the best technology companies, realising that the classic path “study, work hard, buy a home, build a life” is breaking.

This is not a call to “burn everything down” or to idealise any specific party or ideology. It is a call to:

- Look at the data, not just the slogans.

- Recognise that high taxes, restricted land, low social housing and legal noise are not accidents. They are the architecture of the system.

- Stop pretending that only “bad landlords” are the problem, when the State is simultaneously regulator, judge, and one of the biggest financial beneficiaries of high prices.

If you made it this far:

- Share this article if it resonates with you.

- Challenge it if you disagree. But please, with data. I’m Data Scientist 🙂

- And above all, when someone tells you “the problem is your parents’ flat at the beach”, ask them how much the State is collecting every year from housing, how much land is allowed to be built, and why Spain has 3.8 million empty homes and only 3.3% social housing in the middle of an “emergency”.

Because we are not just fighting to buy four walls.

We are fighting for the possibility of building a future that is not already mortgaged before we even start.

Sources and further reading (Spanish)

Quality of life, housing, and social cohesion

- Observatorio de Intangibles y Calidad de Vida (OICV) — artículo sobre vivienda, corrupción y desigualdad social en España (The Conversation / UCLM):

https://doi.org/10.64628/AAO.jr6x3ud4t

Price overvaluation and accessibility

- BIS. Datos de precios de vivienda (serie histórica internacional):

https://www.bis.org/statistics/pp.htm - Artículo sobre la sobrevaloración del 14,3% según el BCE y el 45% de subida real desde 2013 (elEconomista):

https://www.eleconomista.es/vivienda/noticias/13332402/10/25/la-crisis-de-la-vivienda-en-espana-no-tiene-fin-el-bce-detecta-una-rapidisima-sobrevaloracion-de-los-inmuebles.html - Análisis de CaixaBank Research sobre accesibilidad y sobrevaloración por comunidades (incluyendo Madrid y Baleares):

https://www.caixabankresearch.com/es/economia-y-mercados/mercado-inmobiliario

Taxation and fiscal pressure on housing

- Análisis IEE / Foro Consultores sobre fiscalidad de la vivienda, 52.000 millones de recaudación y sobrecoste del 25%:

https://www.foroconsultores.com/blog/2025/05/14/la-fiscalidad-de-la-vivienda-en-espana - Artículo sobre recaudación de 52.000 millones (3,5% del PIB) vía vivienda:

https://www.libertaddigital.com/libremercado/2025-09-02/mar-la-asfixia-al-propietario-de-vivienda-en-espana-solo-por-el-ibi-y-el-iva-se-recaudan-25-000-millones-7290530/ - Datos de recaudación récord por ITP y AJD en comunidades autónomas (ejemplo El País):

https://elpais.com/economia/2025-01-15/las-comunidades-baten-record-de-recaudacion-por-itp-y-ajd-gracias-al-encarecimiento-de-la-vivienda.html

Structural causes and land / planning

- Informe CEU-CEFAS “El problema de la vivienda en España: análisis y propuestas”:

https://fundacionceu.es/cefas/el-problema-de-la-vivienda-en-espana-analisis-y-propuestas/ - Debate sobre suelo urbanizable, planeamiento y restricciones de oferta (ejemplo Reurbanismo / artículos técnicos):

https://www.reurbanismo.es/

Empty homes and “emergency”

- BBC Mundo. “Por qué hay tantas casas vacías en España si el país vive una ‘emergencia habitacional’” (3,8 millones de viviendas vacías, 14,4% del total):

https://www.bbc.com/mundo/articles/c8d5v36z0y5o

Ownership structure and big landlords

- Fotocasa Research. Estudio sobre propietarios: 82% con una sola vivienda, 97% viven en ella:

https://www.fotocasa.es/blog/inmobiliario/estudio-propietarios-vivienda-espana-2024/ - Análisis de Civio sobre grandes tenedores y porcentaje de viviendas en manos de “mega-propietarios”:

https://civio.es/

Social housing and structural deficit

- Informe sobre vivienda social en España (alrededor del 3,3% del parque, frente al 8% europeo). Provivienda:

https://provivienda.org/observatorio/causas-del-problema/parque-de-vivienda/ - Estimaciones de déficit estructural de vivienda y proyección a 2040 (IEE / prensa económica):

https://www.eleconomista.es/vivienda/

Madrid, tourism, and pressure on rents

- Datos de precios y sobrevaloración en Madrid y Baleares (CaixaBank Research / Banco de España): https://www.caixabankresearch.com/es/economia-y-mercados/mercado-inmobiliario

- Estadística experimental. Medición del número de viviendas turísticas en España y su capacidad

https://elpais.com/espana/madrid/

Follow my work

If this topic resonates with you and you want to keep in touch with what I write and build:

- Website: https://cristinavaras.com

- LinkedIn: https://www.linkedin.com/in/cristina-varas

- Medium: https://medium.com/@cristinavaras