A rigorous recap from a curious amateur — and what the evidence suggests we should watch in 2026 (not financial advice).

I’m not a finance professional. I’m simply someone who’s curious about how the world works — and who learns best by turning headlines into a structured, source-backed narrative.

After watching a Spanish video that frames investing as building an “all-terrain” strategy (robust across different macro “weather”), I wanted to sanity-check the big 2025 market story using primary sources and reputable research. If this write-up helps anyone understand 2025 a bit better, I’m happy to share it.

Important disclaimer: this is not investment advice. I do not recommend specific products, allocations, or trades. This is a historical analysis and a scenario framework for what may matter next.

2025 in one sentence

2025 was a year where policy shocks (especially trade policy) repeatedly jolted markets, while monetary policy turned less restrictive, and the year ended with a notable combination of strong risk assets, a weaker dollar, and exceptionally strong precious metals.

The three forces that shaped 2025

1) Trade policy became a first-class market variable again

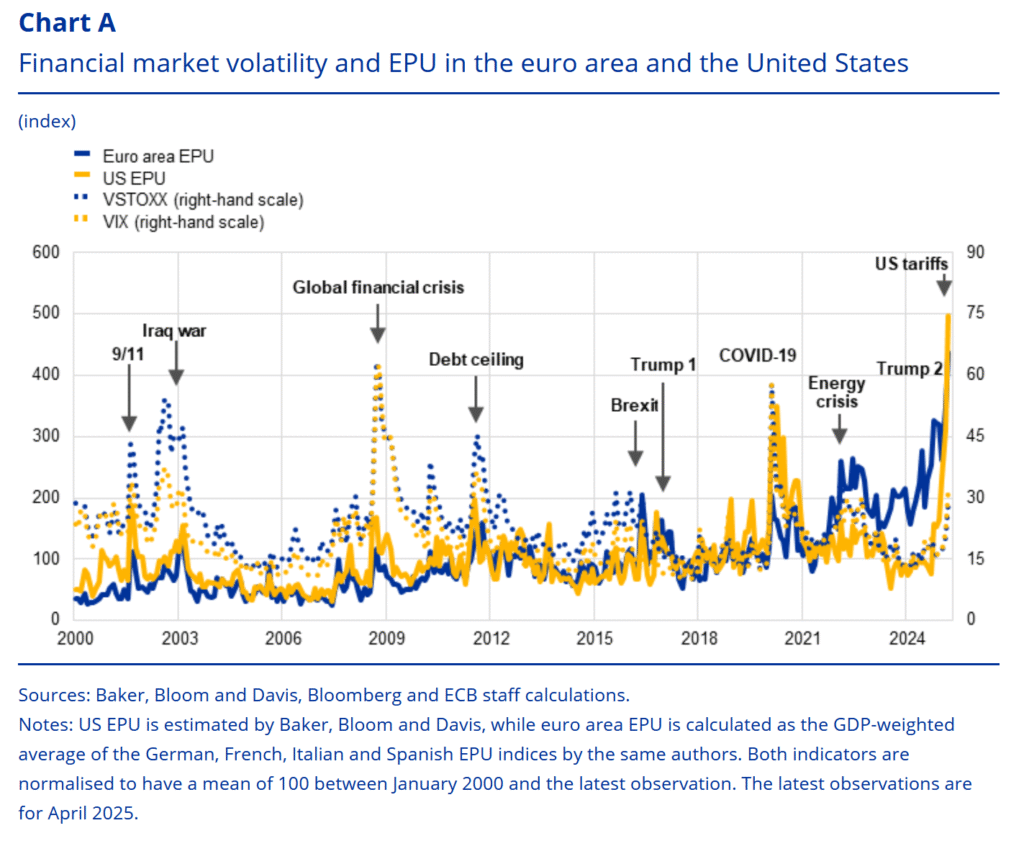

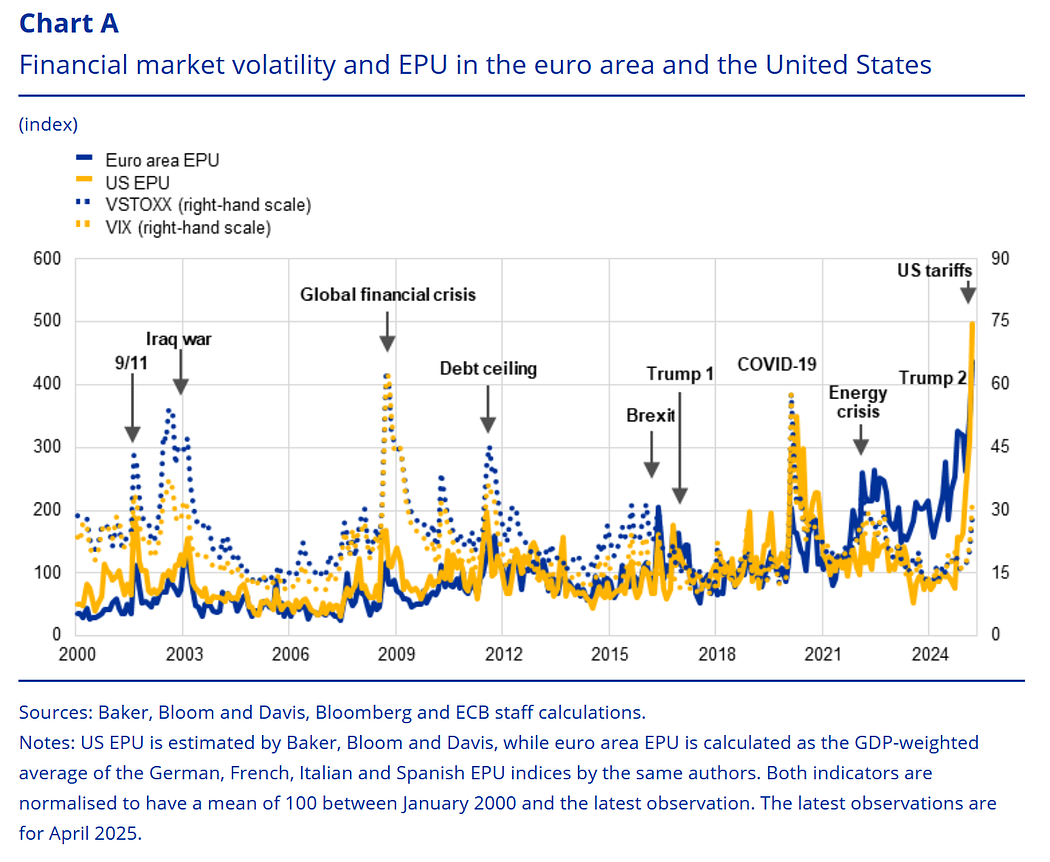

A defining moment was the April 2, 2025 U.S. tariff announcement, which triggered a sharp equity sell-off and a spike in implied volatility (VIX in the U.S. and VSTOXX in Europe).

- ECB analysis explicitly notes that both VIX and VSTOXX spiked following the sell-off triggered by the April 2 tariff announcement:

https://www.ecb.europa.eu/press/economic-bulletin/focus/2025/html/ecb.ebbox202504_05~2dc91bb9e3.en.html

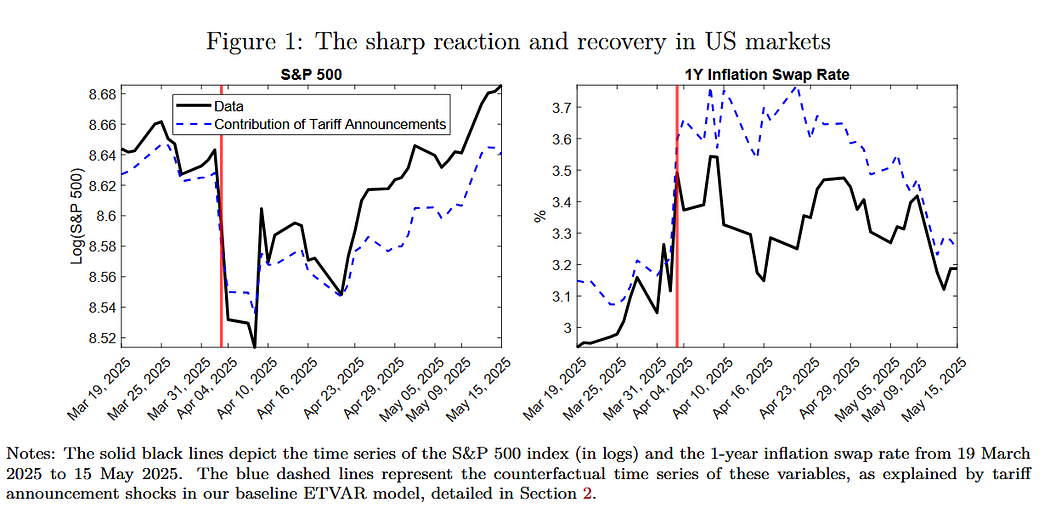

- BIS researchers analyze the March–May 2025 episode and quantify the sharp market reaction and subsequent rebound around the tariff announcements, estimating how much of the move can be attributed to tariff-news shocks in their model:

https://www.bis.org/publ/work1282.htm

Direct PDF: https://www.bis.org/publ/work1282.pdf”

Why this mattered beyond one bad week: in 2025 the market repeatedly demonstrated that policy headlines can dominate the short-term, even when the medium-term fundamentals are improving.

2) Central banks: easing arrived, but the “data dependency” remained

2025 ended with policy rates well below the 2023–2024 peaks, which helped reset the “discount rate” environment. But importantly, communication stayed cautious: central banks kept emphasizing incoming data and risk balance.

Federal Reserve (U.S.)

In December 2025, the FOMC lowered the target range for the federal funds rate to 3.50%–3.75%:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20251210a.htm

Statement PDF: https://www.federalreserve.gov/monetarypolicy/files/monetary20251210a1.pdf

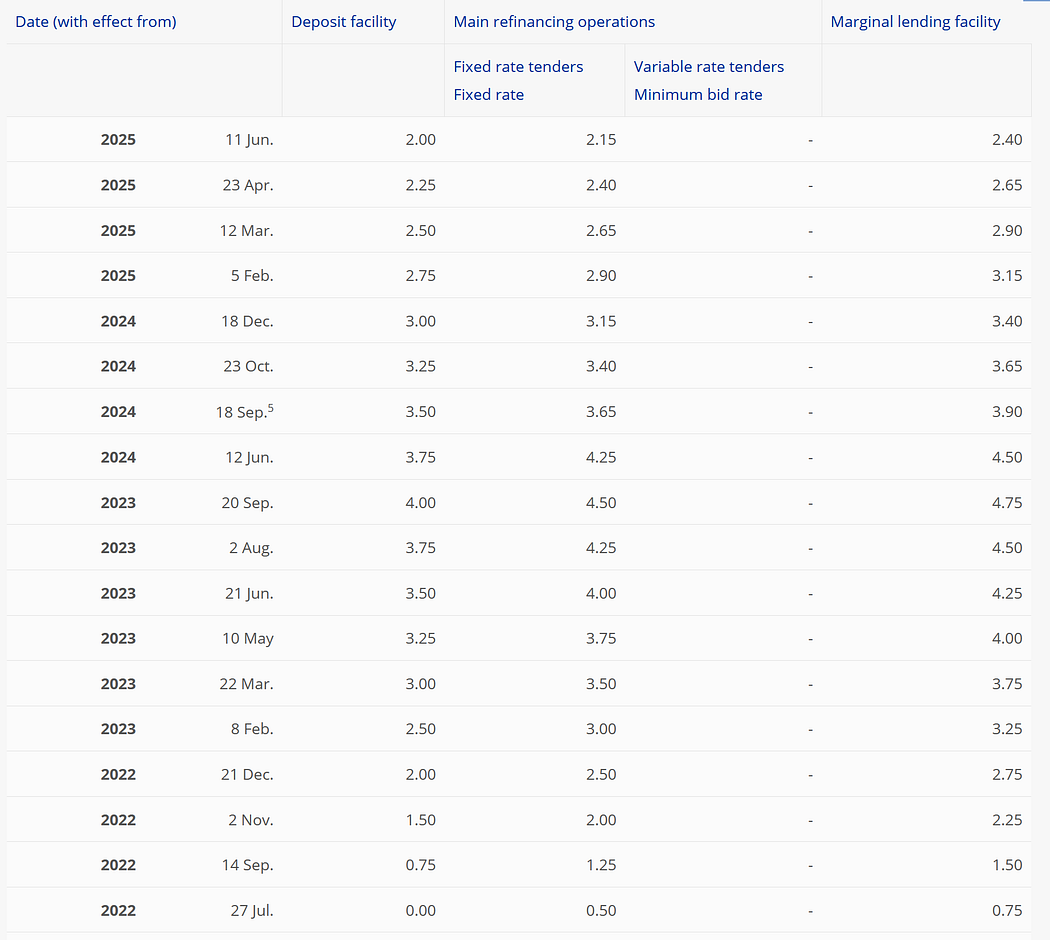

European Central Bank (Euro area)

In December 2025, the ECB left rates unchanged, with the deposit facility at 2.00% (MRO 2.15%, marginal lending 2.40%):

Statement PDF: https://www.ecb.europa.eu/press/press_conference/monetary-policy-statement/shared/pdf/ecb.ds251218~f264376788.en.pdf

Key rates page: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/key_ecb_interest_rates/html/index.en.html

Why this matters for 2026: once rates stop being relentlessly restrictive, markets often shift from “rates are the story” to “growth vs. inflation surprises are the story.” That tends to increase rotation and dispersion across assets.

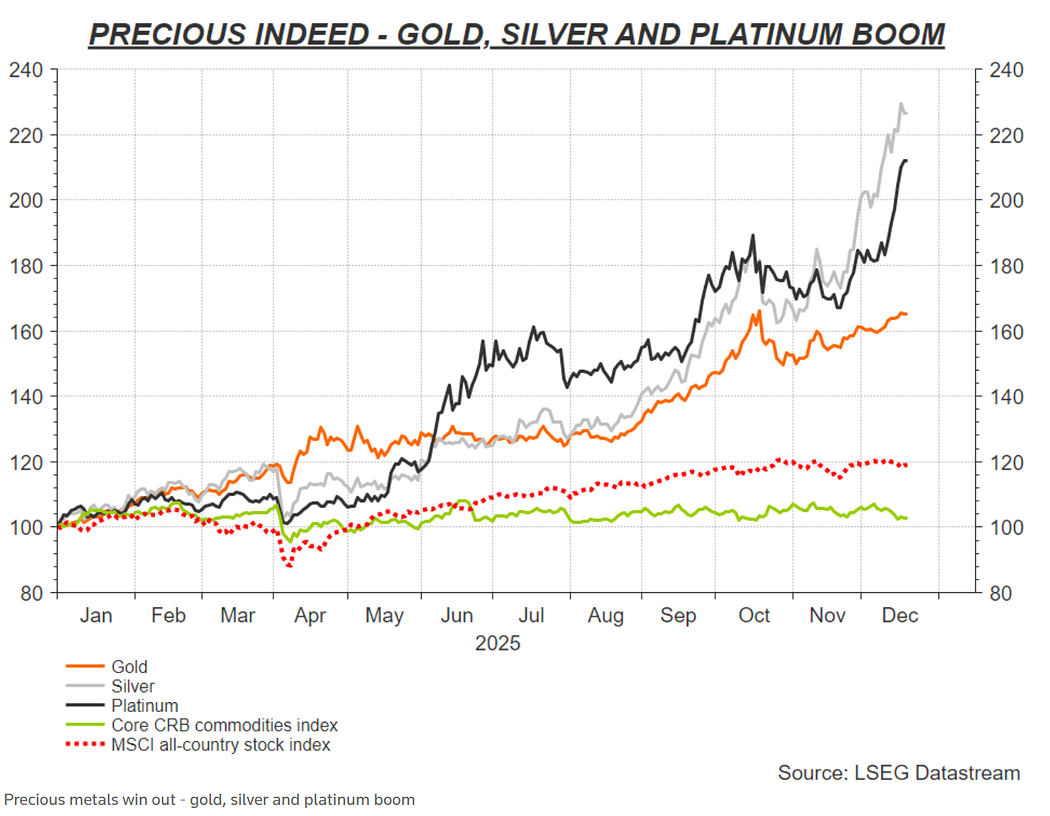

3) The year-end macro signature: a weaker dollar and unusually strong metals

Late December reporting showed a very specific pattern: a sharp annual decline in the U.S. dollar alongside record/near-record precious metals.

- Reuters (Dec 24, 2025): dollar set for its worst year since 2003, down roughly 9–10% on the year:

https://www.reuters.com/world/asia-pacific/dollar-set-worst-year-since-2003-rate-outlooks-diverge-2025-12-24/ - Reuters (Dec 29, 2025): gold tracking toward ~70%+ annual gains (largest since 1979) and silver reaching new highs:

https://www.reuters.com/world/china/global-markets-global-markets-2025-12-29/

- Reuters (Dec 23, 2025): precious metals among top performers in 2025; broader context on “safety trades”:

https://www.reuters.com/markets/global-markets-yearahead-roi-column-graphics-pix-2025-12-23/

Interpretation (non-prescriptive): this combination is consistent with a market that is pricing (a) easing expectations, (b) fiscal uncertainty, and © geopolitical risk — even while equities remain supported.

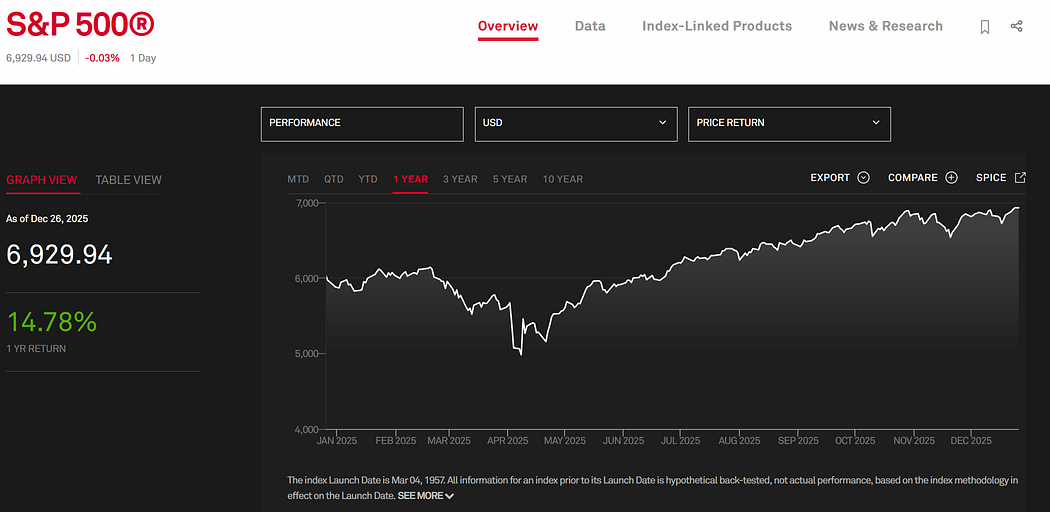

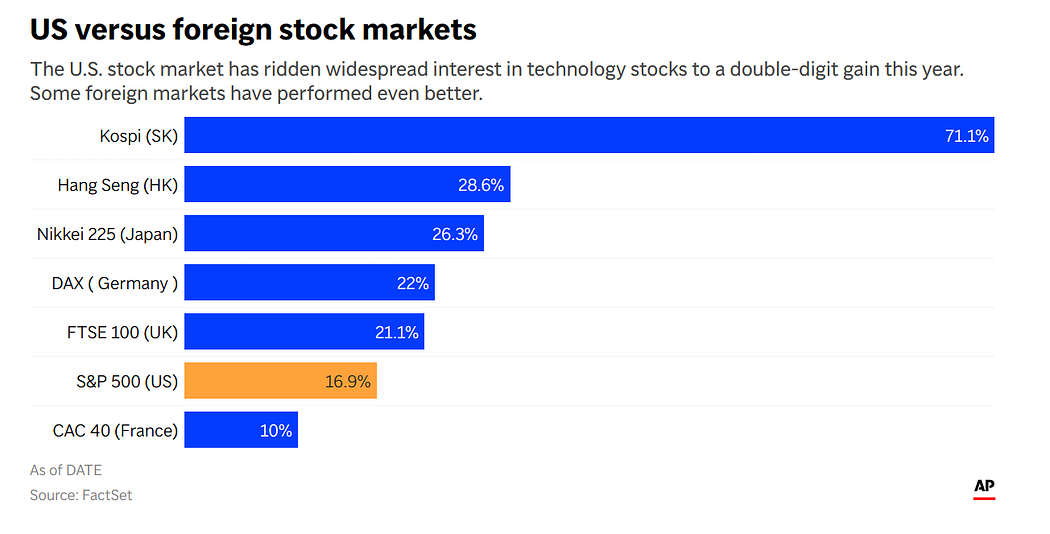

Equities in 2025: strong returns, plus concentration risk in the narrative

U.S. equities ended the year strongly despite sharp drawdowns around policy shocks.

- S&P Dow Jones Indices provides the S&P 500 index overview and performance windows (price return / total return toggles):

https://www.spglobal.com/spdji/en/indices/equity/sp-500/

- AP summary of 2025 performance and the role of tariffs, Fed tension, and AI themes:

https://apnews.com/article/539ae5ec338d19f52116e97d38300c28

One recurring debate in 2025 was concentration (a small set of stocks dominating index performance) and how much of the rally was linked to AI-driven capex and expectations versus broader earnings strength. Even if you disagree with the conclusions, it’s a legitimate question to carry into 2026 because concentration can amplify both upside and downside.

The slow-moving risk: debt, fiscal constraints, and refinancing cost

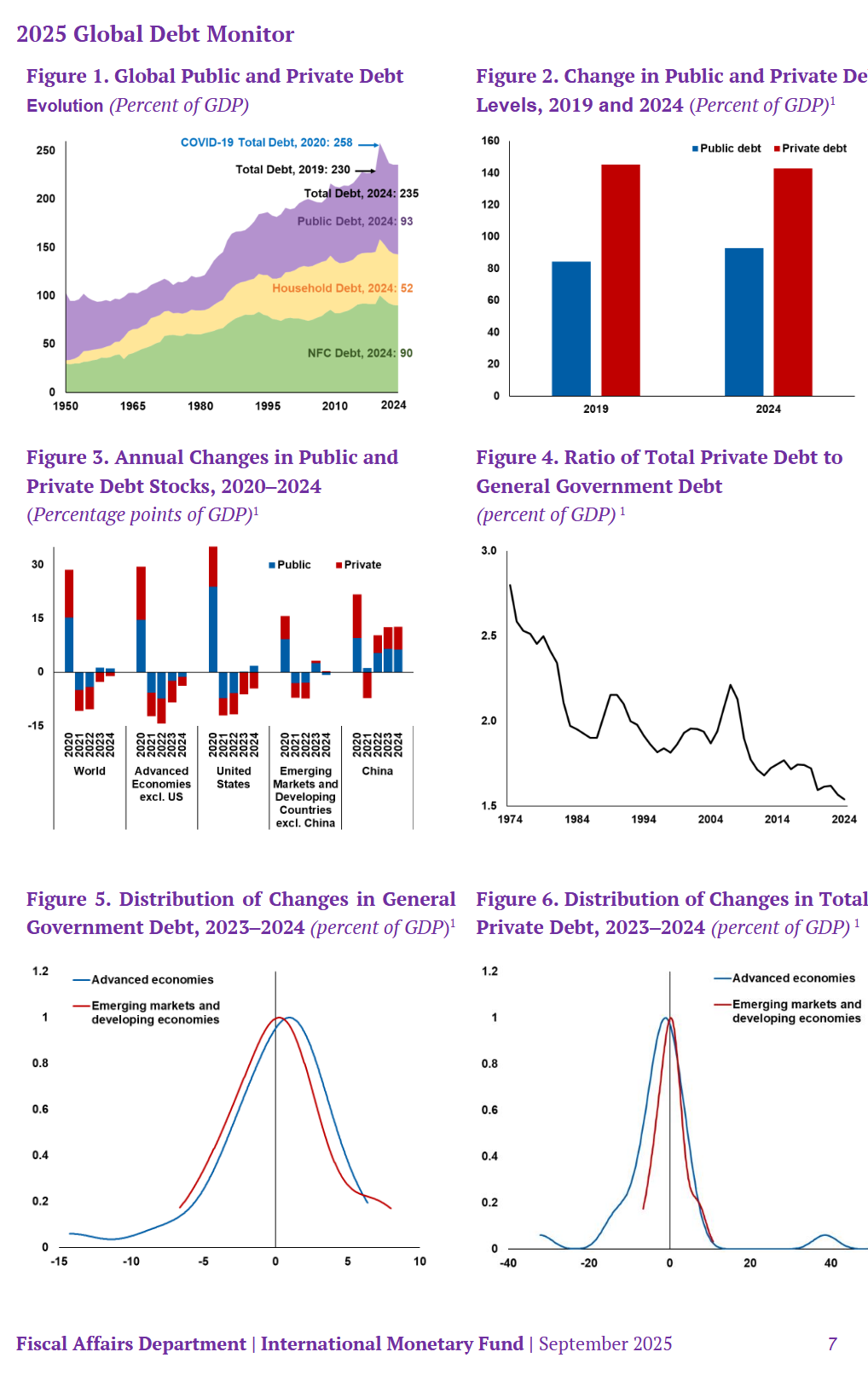

A lot of 2025 commentary referenced global debt levels. The important point is not the viral number; it’s the mechanism:

- higher debt + higher funding costs → greater sensitivity to term premia, auctions, and fiscal credibility.

For a data-centric baseline, the IMF’s Global Debt Monitor is a solid reference:

- IMF Global Debt Monitor 2025 (PDF):

https://www.imf.org/external/datamapper/GDD/2025%20Global%20Debt%20Monitor.pdf

- IMF Fiscal Monitor foreword (Oct 2025) highlighting debt distress and vulnerability even at “moderate” ratios in some countries:

https://www.imf.org/-/media/files/publications/fiscal-monitor/2025/october/english/foreword.pdf

Why this matters for 2026: markets can tolerate high debt for a long time — until they suddenly don’t, usually when liquidity conditions tighten or credibility is questioned. This is one of those “low-frequency, high-impact” variables.

What we can reasonably expect in 2026 (scenario framework, not predictions)

I find it more honest (and more useful) to work in scenarios with observable signposts.

Scenario A: Soft landing + gradual easing (benign base case)

What it looks like: inflation continues to cool; growth slows but holds; central banks ease carefully.

Signposts: inflation prints, labor-market cooling without a sharp break, and central-bank tone (how restrictive they still claim to be).

Scenario B: Policy shock sequel (tariffs, retaliation, fragmentation)

What it looks like: repeated headline-driven repricing; volatility spikes that fade but keep reappearing.

Signposts: new tariff rounds, retaliatory measures, and business confidence indicators turning down.

Scenario C: Fiscal/term-premium repricing

What it looks like: long-end yields rise (or stay sticky) despite easing; credit spreads widen; liquidity risk becomes more visible.

Signposts: weaker auction demand, widening term spreads, and persistent stress indicators.

Scenario D: “Hard-asset bid” persists

What it looks like: metals remain supported by a blend of geopolitics, fiscal uncertainty, and rates/dollar dynamics.

Signposts: real yields, dollar trend, and central-bank reserve behavior.

Scenario E: Equity leadership broadens (or concentration bites)

What it looks like: either the rally becomes more broad-based (healthier breadth) or concentrated leadership becomes a vulnerability in sell-offs.

Signposts: breadth metrics, earnings dispersion, and whether investment translates into productivity (not just narrative).

Closing thought

The most valuable takeaway I’m keeping from 2025 is that the market’s job is not to be calm. It’s to reprice uncertainty. 2025 delivered that lesson via tariffs, central-bank pivots, and a year-end mix of strong equities, a weak dollar, and explosive metals.

If 2026 brings fewer shocks, great. If not, the practical edge is not forecasting perfection. It’s knowing which variables would need to change for your base case to be wrong.

Where to find me

LinkedIn: https://medium.com/@cristina.varas98

Website: https://cristinavaras.com/

If you have a strong source, a correction, or a different interpretation, please leave a comment. I’m always happy to learn and refine the analysis 🙂